What is a Debt Management Plan?

Debt Management Plan, or DMP, is a way to negotiate debt relief with your creditors. The plan, which typically lasts for three to five years, is typically designed to reduce interest rates and eliminate fees.

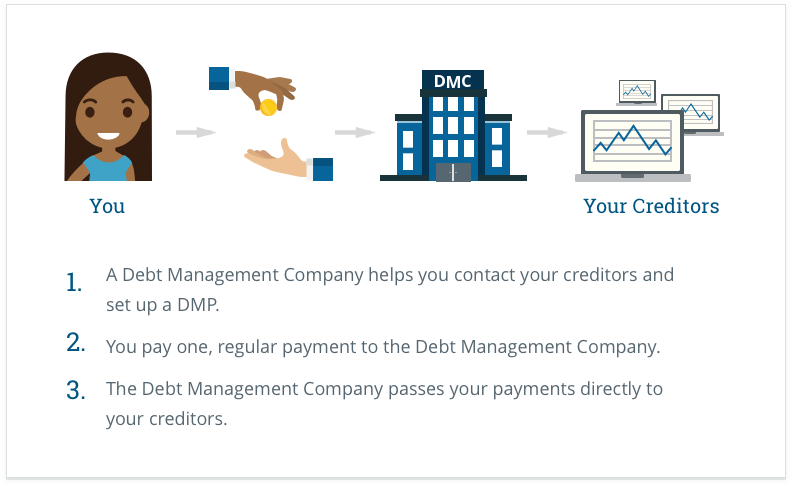

Getting a debt management plan involves contacting a credit counseling agency. This agency will help you create a budget and make a proposal to your creditors. Once you and your creditors agree to the terms, your counselor will work to lower your monthly payments and interest rate. In addition to reducing your debt, this process can raise your credit score.

Some credit card issuers will waive their fees if you enter a debt management program. However, it’s not a good idea to start applying for new credit while you’re involved in a DMP. If you are not able to keep up with your payments, your account may be closed. Not only will this affect your credit score, it can also limit the types of open accounts on your report.

A typical debt management plan costs less than $50 per month. This fee will vary according to state regulations, but can be reduced if you meet certain income requirements. You can sign up for a debt management plan through a nonprofit or for-profit company. Check the Better Business Bureau and your local consumer protection agency to ensure that you are working with a reputable organization.

You will need to pay a setup fee, and a monthly maintenance fee to your counseling agency. These fees can vary from state to state, so you need to know exactly what you’re signing up for before you begin.

When you enter a debt management program, your credit counseling agency will work with your creditors to decrease your interest rates and eliminate fees. They will also send you a monthly progress report. Generally, this will take you at least six months to complete. During this time, your counselor will help you develop a budget and determine what you can afford to spend each month.

Although a debt management plan can improve your financial situation, you should still be responsible with your money. You’ll need to get out of the habit of using credit. Before enrolling in a DMP, close your existing credit cards and avoid applying for any new ones.

Before signing up for a debt management program, you should consult a credit counseling agency for free advice. These organizations are usually nonprofit and have certified counselors. Most of them offer free consultation sessions. Ask about the track record of the company, as well as the success rate of their programs. It’s a good idea to talk to a debt counselor in person, on the phone, or over the internet.

Your debt counselor will work to develop a budget that you can follow. While you’re working with your counselor, you’ll also need to fill out a debt review, which is confidential. You’ll also need to provide your bank account information. After completing this, your counselor will send your creditors a proposal, which they must approve.

What is a Debt Management Plan? was first seen on Apply for an IVA