IVA Debt Help – Choosing an IVA Advisor

Choosing an advisor is an important step in the process. A good IVA advisor will be able to help you determine the best option for your situation. You need to do your homework on the advisor you choose so you are sure they are going to be able to help you. Your advisor will study your debts and let you know which loans you should prioritize.

When it comes to choosing an IP, you should remember that most of them offer an initial meeting for free, but others may require an up-front fee. This fee is typically lost if your IP does not persuade your creditors to accept the proposal. In addition, some IPs will charge you only after the IVA process has started.

If you have an IVA, unsecured creditors cannot repossess your property. However, they can still take legal action against you. You should be vigilant about the actions of your creditors. They may not like your proposal and may even object. An IVA Nominee can apply for an Interim Order, which stops legal action until the Creditors’ Meeting. This order will help you save your home and avoid repossession.

Using an IVA is a great way to protect your assets from creditors and avoid bankruptcy. However, it is not very flexible, and you may not get the best deal for your situation. You should seek out a professional IP to get the best deal. It is also possible to have a modified IVA, but it costs extra.

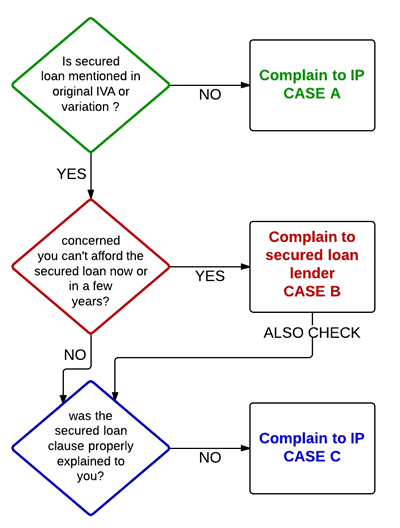

Although an IVA can be damaging to your credit history, it can still be possible to find a bank that will grant you an IVA-friendly loan. In some cases, you can get a good interest rate on an IVA-secured loan. And this is especially useful if you are self-employed.

An Individual Voluntary Arrangement lasts up to five or six years, after which the outstanding balances will be written off. In order to qualify for an IVA, you must have equity in your home, which will be used as collateral. You will need to pay the IVA provider at least PS5,000 to get a secured loan.

IVAs are a legal solution that allows you to pay back your debts in monthly instalments, and the unpaid debts will be written off. An Individual Voluntary Arrangement is set up with a professional debt adviser, who will work out a repayment plan and manage payments to your creditors.

While you may not need to get a secured loan, it will help you raise a large sum of money. With a high-value asset as security, a secured loan can even be obtained by people with poor credit histories. But if you fail to make your repayments, the lender can contact you repeatedly and use debt collectors to threaten you. This can have an impact on your credit score, which can lead to further stress.

Unlike unsecured loans, secured loans do not need Insolvency Practitioner approval. They are often cheaper than unsecured loans, but lenders can reclaim your home if you fail to repay the loan. A secured loan is useful if you need a large sum of money for a major purchase, such as home improvements, university tuition, or debt consolidation.

IVA Debt Help – Choosing an IVA Advisor was first seen on Pathway IT