How Bankruptcy Affects Senior Debt

How Bankruptcy Affects Senior Debt

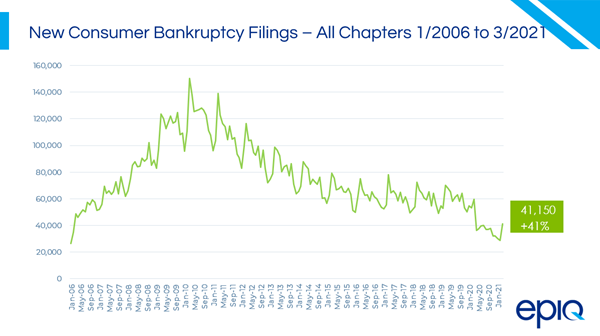

When is a person eligible for Bankruptcy? There are many reasons why taxpayers file for bankruptcy. The best way to avoid bankruptcy is to practice sound financial planning and common sense. If you are contemplating bankruptcy, you may want to consult with a credit counselor or a financial planner. In this article, we will briefly explain the differences between Chapter 7 liquidation and Chapter 13 reorganization and discuss how bankruptcy affects senior debt.

Chapter 7 liquidation

A business can opt for liquidation in bankruptcy through the process. The procedure allows for the discharge of most unsecured debts, such as credit card bills, medical bills, and personal loans. It is the quickest type of bankruptcy, and according to the American Bankruptcy Institute, 63% of Chapter 7 filings were successful, with 94.3% of creditors receiving their full amounts. This method is ideal for those who do not have much property but still owe a lot of debts.

In a Chapter 7 bankruptcy, assets that do not qualify for exemptions can be sold to pay off creditors. These assets may include homes, cars, and other types of property. However, in some cases, the bank is permitted to keep a property if the owner has no equity in it. For these reasons, it is important to know what kinds of assets you can liquidate before filing for bankruptcy. Listed below are some of the most common types of assets.

When choosing a chapter 7 bankruptcy, you must be aware of what your creditors can and cannot recover. The process will start with filing official forms listing the debtor’s financial information, including property ownership. The bankruptcy trustee will then liquidate the property to provide the best return for unsecured creditors. However, if a property is not exempt, the trustee may try to recover some of the money or property through the collection. Ultimately, this process can help you avoid further financial disaster.

Chapter 13 reorganization

If you’re struggling with debt and don’t have a lot of assets, you may be interested in filing for Chapter 13, reorganization in bankruptcy. This type of bankruptcy allows individuals to keep most of their assets but requires the approval of a court. This type of bankruptcy allows you to keep some assets and may even forgive some debts. Listed below are some benefits to filing for Chapter 13 bankruptcy.

One of the biggest benefits of filing for chapter 13 bankruptcy is the chance to save your home. Unlike liquidation under chapter 7, you can use chapter 13 to cure delinquent mortgage payments over a period of time. All you have to do is keep up with your payments over a set period of time. The benefits of a chapter 13 bankruptcy are many. In addition, you can reschedule certain debts, including your mortgage, so that you can make lower payments. You can even make arrangements with third parties, like your employer or landlord.

When filing for Chapter 13 bankruptcy, you must have a detailed plan outlining your repayment schedule. Depending on your assets and income level, you can create a repayment plan that allows you to repay your nondischargeable debts over a three to five-year period. Your repayment plan will need to cover your priority debts. Priority debts are those that are more important than the rest. For example, child support payments or taxes are higher than others. Your plan must include your secured debts as well as any late payments you’ve made.

Senior debt

The two most common forms of senior debt are unsecured credit and secured credit. The former allows creditors to take a secured position over the debtor’s assets. A lien is a legal document that gives a creditor the right to repossess a specific asset in the event that the debtor fails to make repayments on the loan. Liens can be placed on property, vehicles, and equipment. When a business defaults on its debt, these assets are sold to pay the creditors.

If a creditor files a lawsuit, they can seize a person’s assets. Banks often use their assets as collateral. Whether a person is a senior or not, a lawsuit can result in a lien. A lien, or priority of payment, limits a person’s ability to pledge assets for fundraising purposes. In addition, a lien limits the borrower’s ability to pledge their assets without risk of loss.

Senior debt is borrowed money from a company that is supposed to be repaid first in the event of a company’s bankruptcy. Generally, lenders of senior debt are banks that have issued revolving credit lines to a company. In addition, investors typically hold preferred or common stock in a company, which is paid last. When a company declares bankruptcy, its senior debt is first on the list of creditors.

How Bankruptcy Affects Senior Debt was first seen on Apply for an IVA